Monthly Budget Spreadsheet - Easy to Use Budget Spreadsheet for Google Sheets - Free Printable

Educational worksheet: Monthly Budget Spreadsheet - Easy to Use Budget Spreadsheet for Google Sheets. Download and print for classroom or home learning activities.

JPG

1080×1080

153.3 KB

Free · Personal Use

Quality Assured by Worksheets Library Team

Reviewed for educational accuracy and age-appropriateness

ID: #1303241

⭐

Show Answer Key & Explanations

Step-by-step solution for: Monthly Budget Spreadsheet - Easy to Use Budget Spreadsheet for Google Sheets

▼

Show Answer Key & Explanations

Step-by-step solution for: Monthly Budget Spreadsheet - Easy to Use Budget Spreadsheet for Google Sheets

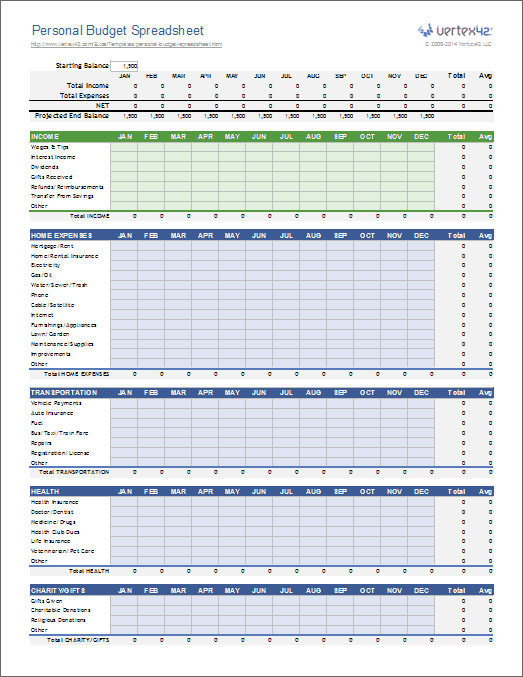

It looks like you've shared an image of a Monthly Budget Spreadsheet template, likely designed for use in Google Sheets, rather than a specific problem or question to solve. This is a promotional graphic showcasing a budgeting tool that helps users track income, expenses, savings, debt, and more.

Since there’s no explicit math problem or task listed in the image (like calculating net income, determining savings goals, or analyzing spending), I’ll assume you're asking for:

> "How does this monthly budget spreadsheet work, and how can it help me manage my finances?"

Let me explain the functionality and benefits of this type of budgeting tool, along with a step-by-step guide on how to use it effectively.

---

This spreadsheet is a comprehensive financial tracker that organizes your money into key categories:

#### 1. Cash Flow Summary

- Shows total income vs. expenses.

- Calculates net cash flow:

`Income - Expenses = Remaining Balance`

- In the example:

- Income: $6,200

- Expenses: $2,750

- Net: $3,450

#### 2. Income Section

- Lists all sources of income (e.g., paycheck, side hustles, dividends).

- Compares planned vs. actual amounts.

- Helps ensure you’re earning what you expect.

#### 3. Bills

- Tracks recurring bills (mortgage, utilities, internet, etc.).

- Includes due dates and planned vs. actual payments.

- Prevents missed payments and late fees.

#### 4. Expenses

- Categorized spending (groceries, gas, dining out, entertainment).

- Allows tracking of planned vs. actual spending.

- Helps identify overspending areas.

#### 5. Savings

- Allocates funds toward goals (emergency fund, vacation, retirement).

- Monitors progress toward savings targets.

#### 6. Debt

- Tracks loan payments (credit cards, student loans, car loans).

- Shows balance reduction over time.

#### 7. Visual Charts

- Pie charts show:

- Income breakdown (where money comes from)

- Expense distribution (how money is spent)

- Actual spending vs. budget

- Bar graphs compare planned vs. actual spending.

#### 8. Additional Features

- Free bill calendar & subscription tracker: Reminds you when bills are due.

- Goals for the month: Set and track personal financial goals (e.g., save $500).

---

1. Input Your Income

- Enter all income sources under “Income.”

- Update each month as needed.

2. List All Bills

- Add monthly bills with due dates.

- Check off when paid.

3. Set Spending Limits

- Plan monthly budgets for categories like groceries, gas, etc.

4. Track Actual Spending

- Record real expenses daily or weekly.

- Compare against planned amounts.

5. Monitor Savings & Debt

- Update savings contributions and debt repayments regularly.

6. Review Monthly

- At the end of each month, analyze:

- Where did you overspend?

- Did you meet savings goals?

- Are bills on schedule?

7. Adjust for Next Month

- Refine your budget based on insights.

---

Let’s say you want to know how much money is left after paying bills and fixed expenses.

From the image:

- Money In: $5,492

- Money Out: $2,750

- Left to Budget: $808 (for variable expenses)

But wait — the "Left to Budget" column shows $808, while the "Left to Spend" shows $3,400.

This discrepancy suggests:

- $808 might be leftover after essential expenses.

- $3,400 could be remaining discretionary spending.

👉 Clarification: The exact meaning depends on how the sheet defines "left to spend." It may include savings or investment allocations.

But if we calculate:

```

Total Income = $6,200

Total Expenses = $2,750

Remaining = $6,200 - $2,750 = $3,450

```

So $3,450 is available for savings, investments, or discretionary spending.

The sheet appears to allocate:

- $808 → flexible spending

- $3,400 → possibly including savings + discretionary

⚠️ There seems to be a labeling inconsistency — double-check how the spreadsheet calculates these numbers.

---

- Use automation: Link Google Sheets to bank accounts via tools like Mint or QuickBooks for automatic updates.

- Set alerts: Use conditional formatting to highlight overspending.

- Back up data: Save copies monthly.

- Review quarterly: Adjust long-term goals.

---

This Monthly Budget Spreadsheet is a powerful tool for:

- Tracking income and expenses

- Avoiding overspending

- Building savings

- Paying down debt

- Reaching financial goals

If you have a specific calculation or scenario you'd like help with (e.g., “How much should I save?” or “Am I on track to pay off my credit card?”), please provide the details, and I’ll walk you through solving it!

Would you like me to create a sample version of this spreadsheet or help you fill it out?

Since there’s no explicit math problem or task listed in the image (like calculating net income, determining savings goals, or analyzing spending), I’ll assume you're asking for:

> "How does this monthly budget spreadsheet work, and how can it help me manage my finances?"

Let me explain the functionality and benefits of this type of budgeting tool, along with a step-by-step guide on how to use it effectively.

---

🔍 Understanding the Monthly Budget Spreadsheet

This spreadsheet is a comprehensive financial tracker that organizes your money into key categories:

#### 1. Cash Flow Summary

- Shows total income vs. expenses.

- Calculates net cash flow:

`Income - Expenses = Remaining Balance`

- In the example:

- Income: $6,200

- Expenses: $2,750

- Net: $3,450

#### 2. Income Section

- Lists all sources of income (e.g., paycheck, side hustles, dividends).

- Compares planned vs. actual amounts.

- Helps ensure you’re earning what you expect.

#### 3. Bills

- Tracks recurring bills (mortgage, utilities, internet, etc.).

- Includes due dates and planned vs. actual payments.

- Prevents missed payments and late fees.

#### 4. Expenses

- Categorized spending (groceries, gas, dining out, entertainment).

- Allows tracking of planned vs. actual spending.

- Helps identify overspending areas.

#### 5. Savings

- Allocates funds toward goals (emergency fund, vacation, retirement).

- Monitors progress toward savings targets.

#### 6. Debt

- Tracks loan payments (credit cards, student loans, car loans).

- Shows balance reduction over time.

#### 7. Visual Charts

- Pie charts show:

- Income breakdown (where money comes from)

- Expense distribution (how money is spent)

- Actual spending vs. budget

- Bar graphs compare planned vs. actual spending.

#### 8. Additional Features

- Free bill calendar & subscription tracker: Reminds you when bills are due.

- Goals for the month: Set and track personal financial goals (e.g., save $500).

---

✔ How to Use This Template Effectively

1. Input Your Income

- Enter all income sources under “Income.”

- Update each month as needed.

2. List All Bills

- Add monthly bills with due dates.

- Check off when paid.

3. Set Spending Limits

- Plan monthly budgets for categories like groceries, gas, etc.

4. Track Actual Spending

- Record real expenses daily or weekly.

- Compare against planned amounts.

5. Monitor Savings & Debt

- Update savings contributions and debt repayments regularly.

6. Review Monthly

- At the end of each month, analyze:

- Where did you overspend?

- Did you meet savings goals?

- Are bills on schedule?

7. Adjust for Next Month

- Refine your budget based on insights.

---

💡 Example Problem: What's Left to Spend?

Let’s say you want to know how much money is left after paying bills and fixed expenses.

From the image:

- Money In: $5,492

- Money Out: $2,750

- Left to Budget: $808 (for variable expenses)

But wait — the "Left to Budget" column shows $808, while the "Left to Spend" shows $3,400.

This discrepancy suggests:

- $808 might be leftover after essential expenses.

- $3,400 could be remaining discretionary spending.

👉 Clarification: The exact meaning depends on how the sheet defines "left to spend." It may include savings or investment allocations.

But if we calculate:

```

Total Income = $6,200

Total Expenses = $2,750

Remaining = $6,200 - $2,750 = $3,450

```

So $3,450 is available for savings, investments, or discretionary spending.

The sheet appears to allocate:

- $808 → flexible spending

- $3,400 → possibly including savings + discretionary

⚠️ There seems to be a labeling inconsistency — double-check how the spreadsheet calculates these numbers.

---

✔ Final Tips

- Use automation: Link Google Sheets to bank accounts via tools like Mint or QuickBooks for automatic updates.

- Set alerts: Use conditional formatting to highlight overspending.

- Back up data: Save copies monthly.

- Review quarterly: Adjust long-term goals.

---

🎯 Conclusion

This Monthly Budget Spreadsheet is a powerful tool for:

- Tracking income and expenses

- Avoiding overspending

- Building savings

- Paying down debt

- Reaching financial goals

If you have a specific calculation or scenario you'd like help with (e.g., “How much should I save?” or “Am I on track to pay off my credit card?”), please provide the details, and I’ll walk you through solving it!

Would you like me to create a sample version of this spreadsheet or help you fill it out?

Parent Tip: Review the logic above to help your child master the concept of free budget spreadsheet.