Rmd Worksheet - Fill and Sign Printable Template Online - Free Printable

Educational worksheet: Rmd Worksheet - Fill and Sign Printable Template Online. Download and print for classroom or home learning activities.

PNG

298×386

11.4 KB

Free · Personal Use

Quality Assured by Worksheets Library Team

Reviewed for educational accuracy and age-appropriateness

ID: #628599

⭐

Show Answer Key & Explanations

Step-by-step solution for: Rmd Worksheet - Fill and Sign Printable Template Online

▼

Show Answer Key & Explanations

Step-by-step solution for: Rmd Worksheet - Fill and Sign Printable Template Online

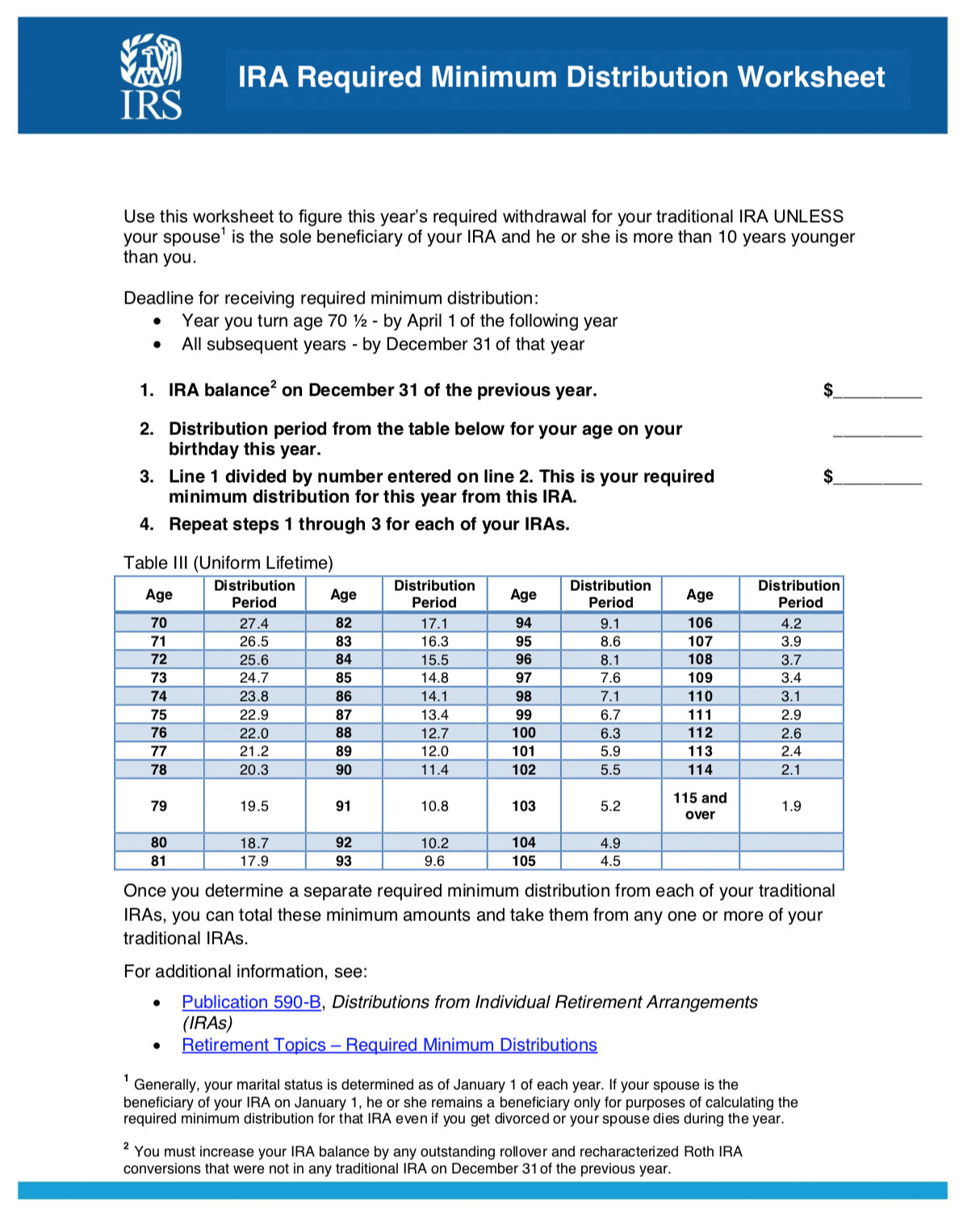

It looks like you've uploaded a worksheet titled "Required Minimum Distribution (RMD) Worksheet" with instructions and steps to calculate Required Minimum Distributions (RMDs) for retirement accounts. However, I don't see an actual image or specific data in your message — just the text of the worksheet.

To help you solve the problem, I’ll walk through how to complete this RMD worksheet step-by-step based on typical IRS rules and the structure of the form. If you have specific account values or dates, please provide them so I can give exact calculations.

---

A Required Minimum Distribution (RMD) is the minimum amount you must withdraw annually from certain retirement accounts (like IRAs and 401(k)s) starting at age 73 (as of 2023, due to SECURE Act changes). Failing to take an RMD results in a 25% penalty.

---

#### STEP A: DETERMINE THE VALUE OF YOUR RETIREMENT ACCOUNTS

> 1.1 Enter the balance of your retirement account as of December 31 of the prior year.

- Example: Suppose your IRA balance on December 31, 2022, was $500,000.

- This is the value used to calculate your 2023 RMD.

> 1.2 If you have multiple accounts (e.g., Traditional IRA, Roth IRA, 401(k)), use the total balance across all eligible accounts.

> ⚠️ Note: You must take RMDs from each account separately, but you can aggregate balances to determine the total RMD if you have multiple IRAs.

---

#### STEP B: DETERMINE THE APPLICABLE LIFE EXPECTANCY

> 2.1 Determine your applicable life expectancy using the IRS Uniform Lifetime Table.

- The IRS provides a Uniform Lifetime Table (found in IRS Publication 590-B).

- Look up your age in the table to find your life expectancy factor.

> Example:

- If you turned 73 in 2023, your life expectancy factor is 25.6 years.

- If you are 74, it's 24.7, etc.

> 2.2 For spouse beneficiaries who are more than 10 years younger than you, use the Joint Life and Last Survivor Expectancy Table instead.

> 2.3 For non-spouse beneficiaries, use the Single Life Expectancy Table.

> 2.4 If you inherited the account and are the beneficiary, different rules apply.

> ❗ Important: Your life expectancy decreases by one year each year after the first RMD.

---

#### STEP C: CALCULATE THE REQUIRED MINIMUM DISTRIBUTION

> 3.1 Use the formula:

\[

\text{RMD} = \frac{\text{Account Balance on Dec 31 of Prior Year}}{\text{Applicable Life Expectancy Factor}}

\]

> Example:

- Account balance: $500,000

- Life expectancy factor: 25.6

- RMD = $500,000 ÷ 25.6 = $19,531.25

> So, you must withdraw at least $19,531.25 by December 31, 2023.

> ⚠️ You can withdraw more, but not less — otherwise, penalties apply.

---

#### Additional Notes

- First RMD is due by April 1 of the year after you turn 73 (for those turning 73 in 2023).

- After that, RMDs are due by December 31 each year.

- If you have multiple IRAs, you can take the total RMD from any one or more of them, but each 401(k) plan requires its own RMD.

---

| Age | Life Expectancy Factor |

|-----|------------------------|

| 73 | 25.6 |

| 74 | 24.7 |

| 75 | 23.8 |

| 76 | 22.9 |

| 77 | 22.0 |

---

Assume:

- You're 73 years old in 2023.

- Your IRA balance on Dec 31, 2022, is $500,000.

- You’re using the Uniform Lifetime Table.

Then:

- RMD for 2023 = $500,000 ÷ 25.6 = $19,531.25

- You must withdraw this amount by April 1, 2024 (first RMD), or December 31, 2023 (if you want to avoid double RMDs).

---

⚠️ Please provide:

- Your age

- Account balance as of Dec 31, prior year

- Whether you’re the original owner or beneficiary

- Type of account (IRA, 401(k), etc.)

And I’ll calculate your exact RMD!

Let me know!

To help you solve the problem, I’ll walk through how to complete this RMD worksheet step-by-step based on typical IRS rules and the structure of the form. If you have specific account values or dates, please provide them so I can give exact calculations.

---

🔍 What is an RMD?

A Required Minimum Distribution (RMD) is the minimum amount you must withdraw annually from certain retirement accounts (like IRAs and 401(k)s) starting at age 73 (as of 2023, due to SECURE Act changes). Failing to take an RMD results in a 25% penalty.

---

✔ Step-by-Step Guide to Completing the RMD Worksheet

#### STEP A: DETERMINE THE VALUE OF YOUR RETIREMENT ACCOUNTS

> 1.1 Enter the balance of your retirement account as of December 31 of the prior year.

- Example: Suppose your IRA balance on December 31, 2022, was $500,000.

- This is the value used to calculate your 2023 RMD.

> 1.2 If you have multiple accounts (e.g., Traditional IRA, Roth IRA, 401(k)), use the total balance across all eligible accounts.

> ⚠️ Note: You must take RMDs from each account separately, but you can aggregate balances to determine the total RMD if you have multiple IRAs.

---

#### STEP B: DETERMINE THE APPLICABLE LIFE EXPECTANCY

> 2.1 Determine your applicable life expectancy using the IRS Uniform Lifetime Table.

- The IRS provides a Uniform Lifetime Table (found in IRS Publication 590-B).

- Look up your age in the table to find your life expectancy factor.

> Example:

- If you turned 73 in 2023, your life expectancy factor is 25.6 years.

- If you are 74, it's 24.7, etc.

> 2.2 For spouse beneficiaries who are more than 10 years younger than you, use the Joint Life and Last Survivor Expectancy Table instead.

> 2.3 For non-spouse beneficiaries, use the Single Life Expectancy Table.

> 2.4 If you inherited the account and are the beneficiary, different rules apply.

> ❗ Important: Your life expectancy decreases by one year each year after the first RMD.

---

#### STEP C: CALCULATE THE REQUIRED MINIMUM DISTRIBUTION

> 3.1 Use the formula:

\[

\text{RMD} = \frac{\text{Account Balance on Dec 31 of Prior Year}}{\text{Applicable Life Expectancy Factor}}

\]

> Example:

- Account balance: $500,000

- Life expectancy factor: 25.6

- RMD = $500,000 ÷ 25.6 = $19,531.25

> So, you must withdraw at least $19,531.25 by December 31, 2023.

> ⚠️ You can withdraw more, but not less — otherwise, penalties apply.

---

#### Additional Notes

- First RMD is due by April 1 of the year after you turn 73 (for those turning 73 in 2023).

- After that, RMDs are due by December 31 each year.

- If you have multiple IRAs, you can take the total RMD from any one or more of them, but each 401(k) plan requires its own RMD.

---

📌 Summary of Key Rules (2023–2024)

| Age | Life Expectancy Factor |

|-----|------------------------|

| 73 | 25.6 |

| 74 | 24.7 |

| 75 | 23.8 |

| 76 | 22.9 |

| 77 | 22.0 |

---

✔ Final Answer Format (Example)

Assume:

- You're 73 years old in 2023.

- Your IRA balance on Dec 31, 2022, is $500,000.

- You’re using the Uniform Lifetime Table.

Then:

- RMD for 2023 = $500,000 ÷ 25.6 = $19,531.25

- You must withdraw this amount by April 1, 2024 (first RMD), or December 31, 2023 (if you want to avoid double RMDs).

---

⚠️ Please provide:

- Your age

- Account balance as of Dec 31, prior year

- Whether you’re the original owner or beneficiary

- Type of account (IRA, 401(k), etc.)

And I’ll calculate your exact RMD!

Let me know!

Parent Tip: Review the logic above to help your child master the concept of required minimum distribution worksheet.

![BLOG] Understanding the IRSs calculations and tables for your ...](/images2/required-minimum-distribution-worksheet/required-minimum-distribution-worksheet-5.png)