Company tax computation format template for financial calculations.

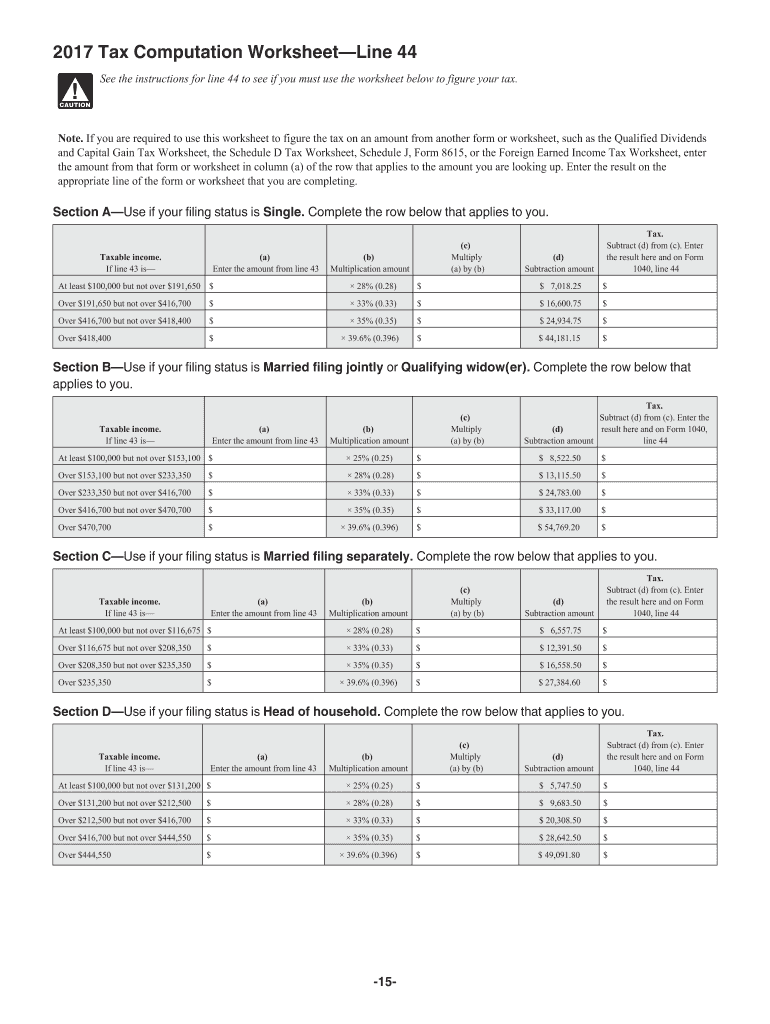

A document titled "COMPANY TAX COMPUTATION - FORMAT" showing a structured table for calculating net profit before tax, non-business income, non-allowable expenses, special deductions, and statutory income, with columns for additions and subtractions in RM.

JPG

495×640

25 KB

Free · Personal Use

Quality Assured by Worksheets Library Team

Reviewed for educational accuracy and age-appropriateness

ID: #265262

⭐

Show Answer Key & Explanations

Step-by-step solution for: Malaysia Personal Income Tax Rates & Table 2012 - Tax Updates ...

▼

Show Answer Key & Explanations

Step-by-step solution for: Malaysia Personal Income Tax Rates & Table 2012 - Tax Updates ...

The image provided is a Company Tax Computation Format used to calculate the taxable income of a company. This format helps in determining the Statutory Income and Aggregate Statutory Income from Businesses, which are crucial for computing the company's tax liability. Below, I will explain the structure and steps involved in solving the problem using this format.

---

#### 1. Net Profit Before Tax

- This is the starting point, representing the company's profit before any adjustments for tax purposes.

- It is typically derived from the Profit and Loss (P&L) statement.

#### 2. Deduct Non-Business Income

- Dividend received: Dividends received by the company are generally not deductible as expenses but may be subject to specific tax treatments.

- Interest received: Interest income earned by the company is also non-deductible for tax purposes.

- Interest on loan to employee: Interest income from loans given to employees is treated similarly.

These items are subtracted because they are considered non-business income and do not qualify as allowable deductions.

#### 3. Add Non-Allowable Expenses

- These are expenses that are incurred but cannot be claimed as deductions for tax purposes:

- Bad Debt: Specific bad debts may be allowed, while general provisions for bad debts are not.

- Depreciation: Depreciation is an allowable expense, so it is added back if it was previously deducted.

- Provision of tax: Tax provisions are not deductible.

- Proposed dividend: Dividends proposed but not yet paid are not deductible.

- Donation: Charitable donations may have specific limits or restrictions.

- Etc.: Other non-allowable expenses.

#### 4. Deduct Special Deduction

- Special deductions are specific expenses allowed under tax laws, such as research and development expenses or other qualifying expenditures. If there are no special deductions, this section remains NIL.

#### 5. Deduct Double Deduction

- Double deductions refer to expenses that have already been deducted elsewhere and should not be claimed again. Examples include approved training costs and insurance premiums.

#### 6. Adjusted Income/Adjusted Loss

- After applying all the above adjustments, the result is the Adjusted Income or Adjusted Loss. This figure represents the company's taxable income after considering non-deductible items and non-allowable expenses.

#### 7. Cap All: Unabsorbed Capital Allowance (CA)

- Unabsorbed CA b/d: Any unutilized capital allowance carried forward from the previous year.

- Current CA: Capital allowances for the current year.

- Balancing Allowance: Additional allowances to balance out certain expenses.

These are subtracted to determine the final adjusted income.

#### 8. Statutory Income

- The Statutory Income is calculated after accounting for all the above adjustments. It represents the taxable income for the current year.

#### 9. Add Statutory Income from Other Business

- If the company has multiple businesses, the statutory income from other businesses is added here.

#### 10. Aggregate Statutory Income from Businesses

- This is the total statutory income from all the company's businesses.

#### 11. Less: Unabsorbed Previous Year Business Loss b/d

- Any business loss carried forward from the previous year can be set off against the current year's income. This reduces the aggregate statutory income.

---

- The Aggregate Statutory Income from Businesses, after deducting the unabsorbed previous year business loss, is the figure used to compute the company's tax liability.

---

1. Non-Business Income: Subtract items like dividends and interest received.

2. Non-Allowable Expenses: Add back items that cannot be deducted for tax purposes.

3. Special Deductions: Include only those expenses specifically allowed under tax laws.

4. Double Deductions: Avoid double-counting expenses.

5. Capital Allowances: Properly account for capital allowances to avoid overdeductions.

6. Previous Year Losses: Use unabsorbed losses to reduce the current year's taxable income.

---

To solve the problem using this format:

1. Start with the Net Profit Before Tax.

2. Subtract Non-Business Income.

3. Add back Non-Allowable Expenses.

4. Subtract Special Deductions and Double Deductions.

5. Calculate the Adjusted Income/Adjusted Loss.

6. Account for Cap All: Unabsorbed CA.

7. Determine the Statutory Income.

8. Add Statutory Income from Other Business.

9. Compute the Aggregate Statutory Income from Businesses.

10. Subtract the Unabsorbed Previous Year Business Loss.

The final result is the Aggregate Statutory Income from Businesses, which is the basis for calculating the company's tax liability.

---

\[

\boxed{\text{Aggregate Statutory Income from Businesses}}

\]

---

Step-by-Step Explanation

#### 1. Net Profit Before Tax

- This is the starting point, representing the company's profit before any adjustments for tax purposes.

- It is typically derived from the Profit and Loss (P&L) statement.

#### 2. Deduct Non-Business Income

- Dividend received: Dividends received by the company are generally not deductible as expenses but may be subject to specific tax treatments.

- Interest received: Interest income earned by the company is also non-deductible for tax purposes.

- Interest on loan to employee: Interest income from loans given to employees is treated similarly.

These items are subtracted because they are considered non-business income and do not qualify as allowable deductions.

#### 3. Add Non-Allowable Expenses

- These are expenses that are incurred but cannot be claimed as deductions for tax purposes:

- Bad Debt: Specific bad debts may be allowed, while general provisions for bad debts are not.

- Depreciation: Depreciation is an allowable expense, so it is added back if it was previously deducted.

- Provision of tax: Tax provisions are not deductible.

- Proposed dividend: Dividends proposed but not yet paid are not deductible.

- Donation: Charitable donations may have specific limits or restrictions.

- Etc.: Other non-allowable expenses.

#### 4. Deduct Special Deduction

- Special deductions are specific expenses allowed under tax laws, such as research and development expenses or other qualifying expenditures. If there are no special deductions, this section remains NIL.

#### 5. Deduct Double Deduction

- Double deductions refer to expenses that have already been deducted elsewhere and should not be claimed again. Examples include approved training costs and insurance premiums.

#### 6. Adjusted Income/Adjusted Loss

- After applying all the above adjustments, the result is the Adjusted Income or Adjusted Loss. This figure represents the company's taxable income after considering non-deductible items and non-allowable expenses.

#### 7. Cap All: Unabsorbed Capital Allowance (CA)

- Unabsorbed CA b/d: Any unutilized capital allowance carried forward from the previous year.

- Current CA: Capital allowances for the current year.

- Balancing Allowance: Additional allowances to balance out certain expenses.

These are subtracted to determine the final adjusted income.

#### 8. Statutory Income

- The Statutory Income is calculated after accounting for all the above adjustments. It represents the taxable income for the current year.

#### 9. Add Statutory Income from Other Business

- If the company has multiple businesses, the statutory income from other businesses is added here.

#### 10. Aggregate Statutory Income from Businesses

- This is the total statutory income from all the company's businesses.

#### 11. Less: Unabsorbed Previous Year Business Loss b/d

- Any business loss carried forward from the previous year can be set off against the current year's income. This reduces the aggregate statutory income.

---

Final Output

- The Aggregate Statutory Income from Businesses, after deducting the unabsorbed previous year business loss, is the figure used to compute the company's tax liability.

---

Key Points to Remember

1. Non-Business Income: Subtract items like dividends and interest received.

2. Non-Allowable Expenses: Add back items that cannot be deducted for tax purposes.

3. Special Deductions: Include only those expenses specifically allowed under tax laws.

4. Double Deductions: Avoid double-counting expenses.

5. Capital Allowances: Properly account for capital allowances to avoid overdeductions.

6. Previous Year Losses: Use unabsorbed losses to reduce the current year's taxable income.

---

Solution Summary

To solve the problem using this format:

1. Start with the Net Profit Before Tax.

2. Subtract Non-Business Income.

3. Add back Non-Allowable Expenses.

4. Subtract Special Deductions and Double Deductions.

5. Calculate the Adjusted Income/Adjusted Loss.

6. Account for Cap All: Unabsorbed CA.

7. Determine the Statutory Income.

8. Add Statutory Income from Other Business.

9. Compute the Aggregate Statutory Income from Businesses.

10. Subtract the Unabsorbed Previous Year Business Loss.

The final result is the Aggregate Statutory Income from Businesses, which is the basis for calculating the company's tax liability.

---

Final Answer

\[

\boxed{\text{Aggregate Statutory Income from Businesses}}

\]

Parent Tip: Review the logic above to help your child master the concept of tax computation worksheet 2012.