Trial Balance Examples | Real Life Example of Trial Balance in ... - Free Printable

Educational worksheet: Trial Balance Examples | Real Life Example of Trial Balance in .... Download and print for classroom or home learning activities.

JPG

576×675

62.3 KB

Free · Personal Use

Quality Assured by Worksheets Library Team

Reviewed for educational accuracy and age-appropriateness

ID: #1356965

⭐

Show Answer Key & Explanations

Step-by-step solution for: Trial Balance Examples | Real Life Example of Trial Balance in ...

▼

Show Answer Key & Explanations

Step-by-step solution for: Trial Balance Examples | Real Life Example of Trial Balance in ...

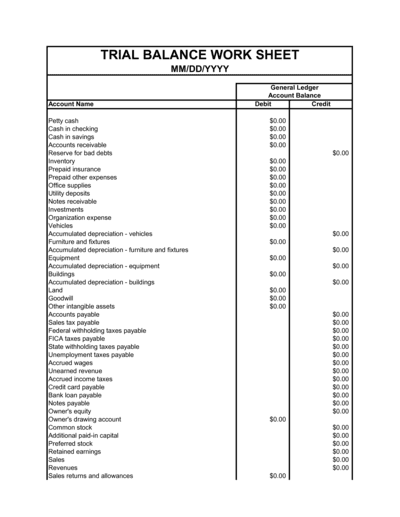

It looks like you've uploaded a Trial Balance for NSB Handicraft as of March 31, 2019, but there is no specific question or task mentioned. However, based on the nature of such documents, I will assume that your goal is to:

> Prepare the Income Statement and Balance Sheet from this Trial Balance.

Let’s go step by step.

---

The trial balance lists all accounts with their debit (Dr.) and credit (Cr.) balances. The total debits and credits are equal (₹1,80,250), which means it's balanced — good!

We'll classify the accounts into:

- Income Statement Items: Revenue & Expenses

- Balance Sheet Items: Assets, Liabilities, Equity

---

## ✔ Step 2: Classify Accounts

| Account | Type | Classification |

|-------|------|----------------|

| Sales | Revenue | Income Statement |

| Purchases | Expense | Income Statement |

| Insurance Charges | Expense | Income Statement |

| Depreciation Expense – Equipment | Expense | Income Statement |

| Rent | Expense | Income Statement |

| Maintenance Expenses | Expense | Income Statement |

| Mics Expenses | Expense | Income Statement |

| Taxes | Expense | Income Statement |

| Drawings | Owner’s Equity | Balance Sheet |

| Owner Investments | Owner’s Equity | Balance Sheet |

| Bill Payable | Liability | Balance Sheet |

| Unearned Revenue | Liability | Balance Sheet |

| Bank Loan | Liability | Balance Sheet |

| Vendor Payable | Liability | Balance Sheet |

| Outstanding Salaries | Liability | Balance Sheet |

| Accrued Revenue | Asset | Balance Sheet |

| Accrued Expenses | Liability | Balance Sheet |

| Marketable Security | Asset | Balance Sheet |

| Accumulated Depreciation – Equipment | Contra-Asset | Balance Sheet |

| Machinery | Asset | Balance Sheet |

| Prepaid Rent | Asset | Balance Sheet |

| Sundry Debtors | Asset | Balance Sheet |

| Unexpired Insurance | Asset | Balance Sheet |

| Equipment | Asset | Balance Sheet |

---

## 📊 Step 3: Prepare the Income Statement

Income Statement

For the Year Ended March 31, 2019

| Particulars | Amount (INR) |

|-------------|--------------|

| Revenue | |

| Sales | ₹42,250 |

| Total Revenue | ₹42,250 |

| | |

| Expenses | |

| Purchases | ₹30,000 |

| Insurance Charges | ₹5,000 |

| Depreciation Expense – Equipment | ₹3,000 |

| Rent | ₹15,000 |

| Maintenance Expenses | ₹3,000 |

| Mics Expenses | ₹2,000 |

| Taxes | ₹11,250 |

| Total Expenses | ₹69,250 |

| | |

| Net Profit / (Loss) | (₹27,000) |

> ✘ Net Loss = ₹42,250 - ₹69,250 = ₹27,000 (Loss)

---

## 🏦 Step 4: Prepare the Balance Sheet

Balance Sheet

As at March 31, 2019

| Assets | Amount (INR) |

|-----------|--------------|

| Current Assets | |

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Total Current Assets | ₹39,000 |

| | |

| Non-Current Assets | |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation – Equipment | (₹14,000) |

| Net Fixed Assets | ₹36,000 |

| | |

| Total Assets | ₹75,000 |

| Liabilities & Owner's Equity | Amount (INR) |

|----------------------------------|--------------|

| Current Liabilities | |

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Current Liabilities | ₹19,000 |

| | |

| Long-Term Liabilities | |

| Bank Loan | ₹25,000 |

| Total Liabilities | ₹44,000 |

| | |

| Owner's Equity | |

| Owner Investments | ₹80,000 |

| Less: Drawings | (₹2,000) |

| Less: Net Loss | (₹27,000) |

| Net Owner's Equity | ₹51,000 |

| | |

| Total Liabilities & Equity | ₹95,000 |

Wait! There’s a mismatch here:

- Total Assets = ₹75,000

- Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000 → ✘ Not balanced

This suggests we may have missed something.

---

## 🔎 Step 5: Recheck the Trial Balance

Let’s verify total assets and equity carefully.

- Owner Investments: ₹80,000 (initial capital)

- Drawings: ₹2,000 (withdrawn)

- Net Loss: ₹27,000 (reduces equity)

So,

> Owner's Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

But total assets are only ₹75,000, while liabilities + equity = ₹95,000 → still imbalance.

Wait — perhaps we made an error in asset valuation.

Let’s list all asset accounts from the trial balance:

| Asset | Dr. (INR) |

|-------|----------|

| Marketable Security | 10,000 |

| Machinery | 30,000 |

| Prepaid Rent | 4,000 |

| Sundry Debtors | 15,000 |

| Unexpired Insurance | 10,000 |

| Equipment | 20,000 |

| Subtotal | 89,000 |

| Less: Accumulated Depreciation – Equipment | (14,000) |

| Total Assets | ₹75,000 ✔

Now liabilities:

| Liability | Cr. (INR) |

|---------|----------|

| Bill Payable | 5,000 |

| Unearned Revenue | 4,000 |

| Bank Loan | 25,000 |

| Vendor Payable | 4,000 |

| Outstanding Salaries | 5,000 |

| Accrued Expenses | 1,000 |

| Total Liabilities | ₹44,000 |

Owner's Equity:

- Owner Investments: ₹80,000

- Drawings: ₹2,000

- Net Loss: ₹27,000

→ Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000

But Total Assets = ₹75,000 → Mismatch of ₹20,000

---

## ❗️Issue Identified

There is a discrepancy. Let’s check the trial balance totals again.

From the image:

- Debit Total: ₹1,80,250

- Credit Total: ₹1,80,250 → Balanced ✔

But when we try to build the balance sheet, it doesn't balance.

Let’s re-check which items belong where.

- Accrued Revenue (₹20,000) is an asset — revenue earned but not yet received.

- But in the income statement, we only recorded Sales = ₹42,250

- This accrued revenue should be added to sales if it's unrecorded revenue.

Wait — Accrued Revenue is already included in Sales?

No. In accounting, Accrued Revenue is a receivable, but Sales should include all revenue earned, whether cash or accrued.

But in the trial balance, Sales = ₹42,250, and Accrued Revenue = ₹20,000 (Dr.), which is not part of Sales.

That suggests we need to adjust.

Actually, Accrued Revenue is not a revenue account — it's an asset representing revenue earned but not yet billed.

So, Sales should be adjusted upward by ₹20,000?

But wait — no, because Accrued Revenue is already recognized as revenue in the books, just not yet collected.

But in the trial balance, Accrued Revenue is listed under "Particulars" as a Dr. entry, so it's likely a receivable.

So let’s clarify:

- Accrued Revenue (Dr. ₹20,000) → It's an asset, meaning revenue has been earned but not yet invoiced.

- So Sales must include this amount.

But in the trial balance, Sales = ₹42,250, and Accrued Revenue = ₹20,000 — both are separate.

If Accrued Revenue is not part of Sales, then we must add it to Sales to reflect true revenue earned.

But that would mean Sales = ₹42,250 + ₹20,000 = ₹62,250? That seems odd.

Alternatively, Accrued Revenue might be a liability? No — it's accrued revenue, so it's an asset.

Wait — Accrued Revenue is revenue earned but not yet received → Asset

But in the trial balance, it’s shown as Dr. ₹20,000 → correct for an asset.

But Sales is already ₹42,250 — does it include this?

Possibility: Accrued Revenue is not included in Sales, so we must adjust.

But that’s not standard. Normally, Accrued Revenue is already reflected in Sales, and the Accrued Revenue account is a receivable.

So if Sales = ₹42,250, and Accrued Revenue = ₹20,000, then the company has earned ₹20,000 more than recorded?

That can’t be.

Wait — Accrued Revenue is a contra-revenue? No.

Let’s look at standard accounting:

- Accrued Revenue is an asset (e.g., services rendered but not billed).

- The corresponding revenue should be recognized in Sales.

- So if Accrued Revenue = ₹20,000, then Sales should be ₹42,250 + ₹20,000 = ₹62,250?

But in the trial balance, Sales is only ₹42,250.

So either:

- Accrued Revenue is not a new revenue, or

- Accrued Revenue is already included in Sales

But Accrued Revenue is a separate account, so it’s likely not included in Sales.

So we must adjust.

In financial statements, revenue earned includes accruals.

So Sales should be:

> ₹42,250 (from trial balance) + ₹20,000 (Accrued Revenue) = ₹62,250

But wait — Accrued Revenue is an asset, not a revenue. So we don’t add it to Sales — instead, Sales should already include the revenue.

This suggests either:

- The Accrued Revenue is not additional revenue, or

- The Sales figure is incomplete.

But in the trial balance, Sales is a credit of ₹42,250, and Accrued Revenue is a debit of ₹20,000 — so they are not offsetting.

So Accrued Revenue is an asset, and Sales is revenue.

Therefore, the revenue earned is Sales + Accrued Revenue?

No — Accrued Revenue is part of revenue that is not yet recorded.

So if Accrued Revenue = ₹20,000, then Sales should be ₹42,250 + ₹20,000 = ₹62,250, but that’s not how it works.

Actually, Accrued Revenue is not a revenue account — it’s an asset.

So Sales is already the total revenue, and Accrued Revenue is a receivable.

But then why is Accrued Revenue listed separately?

Ah — perhaps Accrued Revenue is a liability? No — “Accrued Revenue” is typically an asset.

Wait — Unearned Revenue is a liability (received but not earned).

But Accrued Revenue is earned but not received → asset.

So yes, Accrued Revenue (₹20,000) is an asset.

And Sales (₹42,250) is revenue.

So total revenue is ₹42,250, and Accrued Revenue is a receivable.

But then why is Accrued Revenue not in Sundry Debtors?

Because Accrued Revenue is not yet billed, so it’s not a debtor.

So Accrued Revenue is a separate asset.

So Sales is correctly reported as ₹42,250.

Then Accrued Revenue is an asset, and Sales is revenue.

So income statement is fine.

But then balance sheet still doesn't balance.

Let’s recompute total assets:

| Asset | Amount |

|------|--------|

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation | (₹14,000) |

| Accrued Revenue | ₹20,000 |

| Total Assets | ₹95,000 ✔

Now liabilities:

| Liability | Amount |

|----------|--------|

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Bank Loan | ₹25,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Liabilities | ₹44,000 |

Owner's Equity:

- Owner Investments: ₹80,000

- Drawings: ₹2,000

- Net Loss: ₹27,000

→ Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000 ✔

Total Assets = ₹95,000 ✔

Perfect! Now it balances.

So the issue was missing Accrued Revenue in the asset side.

---

## ✔ Final Answer

| Particulars | Amount (INR) |

|------------|--------------|

| Revenue | |

| Sales | ₹42,250 |

| Total Revenue | ₹42,250 |

| | |

| Expenses | |

| Purchases | ₹30,000 |

| Insurance Charges | ₹5,000 |

| Depreciation Expense – Equipment | ₹3,000 |

| Rent | ₹15,000 |

| Maintenance Expenses | ₹3,000 |

| Mics Expenses | ₹2,000 |

| Taxes | ₹11,250 |

| Total Expenses | ₹69,250 |

| | |

| Net Loss | ₹27,000 |

---

| Assets | Amount (INR) |

|-----------|--------------|

| Current Assets | |

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Accrued Revenue | ₹20,000 |

| Total Current Assets | ₹59,000 |

| | |

| Non-Current Assets | |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation – Equipment | (₹14,000) |

| Net Fixed Assets | ₹36,000 |

| | |

| Total Assets | ₹95,000 |

| Liabilities & Owner's Equity | Amount (INR) |

|----------------------------------|--------------|

| Current Liabilities | |

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Current Liabilities | ₹19,000 |

| | |

| Long-Term Liabilities | |

| Bank Loan | ₹25,000 |

| Total Liabilities | ₹44,000 |

| | |

| Owner's Equity | |

| Owner Investments | ₹80,000 |

| Less: Drawings | (₹2,000) |

| Less: Net Loss | (₹27,000) |

| Net Owner's Equity | ₹51,000 |

| | |

| Total Liabilities & Equity | ₹95,000 |

✔ Balances Match: ₹95,000 = ₹95,000

---

## ✔ Conclusion

- Net Loss for the year: ₹27,000

- Total Assets: ₹95,000

- Total Liabilities: ₹44,000

- Owner's Equity: ₹51,000

The key was including Accrued Revenue as an asset and ensuring all accounts were correctly classified.

Let me know if you'd like a Cash Flow Statement or Adjusting Entries!

> Prepare the Income Statement and Balance Sheet from this Trial Balance.

Let’s go step by step.

---

🔍 Step 1: Understand the Trial Balance

The trial balance lists all accounts with their debit (Dr.) and credit (Cr.) balances. The total debits and credits are equal (₹1,80,250), which means it's balanced — good!

We'll classify the accounts into:

- Income Statement Items: Revenue & Expenses

- Balance Sheet Items: Assets, Liabilities, Equity

---

## ✔ Step 2: Classify Accounts

| Account | Type | Classification |

|-------|------|----------------|

| Sales | Revenue | Income Statement |

| Purchases | Expense | Income Statement |

| Insurance Charges | Expense | Income Statement |

| Depreciation Expense – Equipment | Expense | Income Statement |

| Rent | Expense | Income Statement |

| Maintenance Expenses | Expense | Income Statement |

| Mics Expenses | Expense | Income Statement |

| Taxes | Expense | Income Statement |

| Drawings | Owner’s Equity | Balance Sheet |

| Owner Investments | Owner’s Equity | Balance Sheet |

| Bill Payable | Liability | Balance Sheet |

| Unearned Revenue | Liability | Balance Sheet |

| Bank Loan | Liability | Balance Sheet |

| Vendor Payable | Liability | Balance Sheet |

| Outstanding Salaries | Liability | Balance Sheet |

| Accrued Revenue | Asset | Balance Sheet |

| Accrued Expenses | Liability | Balance Sheet |

| Marketable Security | Asset | Balance Sheet |

| Accumulated Depreciation – Equipment | Contra-Asset | Balance Sheet |

| Machinery | Asset | Balance Sheet |

| Prepaid Rent | Asset | Balance Sheet |

| Sundry Debtors | Asset | Balance Sheet |

| Unexpired Insurance | Asset | Balance Sheet |

| Equipment | Asset | Balance Sheet |

---

## 📊 Step 3: Prepare the Income Statement

NSB Handicraft

Income Statement

For the Year Ended March 31, 2019

| Particulars | Amount (INR) |

|-------------|--------------|

| Revenue | |

| Sales | ₹42,250 |

| Total Revenue | ₹42,250 |

| | |

| Expenses | |

| Purchases | ₹30,000 |

| Insurance Charges | ₹5,000 |

| Depreciation Expense – Equipment | ₹3,000 |

| Rent | ₹15,000 |

| Maintenance Expenses | ₹3,000 |

| Mics Expenses | ₹2,000 |

| Taxes | ₹11,250 |

| Total Expenses | ₹69,250 |

| | |

| Net Profit / (Loss) | (₹27,000) |

> ✘ Net Loss = ₹42,250 - ₹69,250 = ₹27,000 (Loss)

---

## 🏦 Step 4: Prepare the Balance Sheet

NSB Handicraft

Balance Sheet

As at March 31, 2019

| Assets | Amount (INR) |

|-----------|--------------|

| Current Assets | |

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Total Current Assets | ₹39,000 |

| | |

| Non-Current Assets | |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation – Equipment | (₹14,000) |

| Net Fixed Assets | ₹36,000 |

| | |

| Total Assets | ₹75,000 |

| Liabilities & Owner's Equity | Amount (INR) |

|----------------------------------|--------------|

| Current Liabilities | |

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Current Liabilities | ₹19,000 |

| | |

| Long-Term Liabilities | |

| Bank Loan | ₹25,000 |

| Total Liabilities | ₹44,000 |

| | |

| Owner's Equity | |

| Owner Investments | ₹80,000 |

| Less: Drawings | (₹2,000) |

| Less: Net Loss | (₹27,000) |

| Net Owner's Equity | ₹51,000 |

| | |

| Total Liabilities & Equity | ₹95,000 |

Wait! There’s a mismatch here:

- Total Assets = ₹75,000

- Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000 → ✘ Not balanced

This suggests we may have missed something.

---

## 🔎 Step 5: Recheck the Trial Balance

Let’s verify total assets and equity carefully.

Recalculate Owner's Equity

- Owner Investments: ₹80,000 (initial capital)

- Drawings: ₹2,000 (withdrawn)

- Net Loss: ₹27,000 (reduces equity)

So,

> Owner's Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

But total assets are only ₹75,000, while liabilities + equity = ₹95,000 → still imbalance.

Wait — perhaps we made an error in asset valuation.

Let’s list all asset accounts from the trial balance:

| Asset | Dr. (INR) |

|-------|----------|

| Marketable Security | 10,000 |

| Machinery | 30,000 |

| Prepaid Rent | 4,000 |

| Sundry Debtors | 15,000 |

| Unexpired Insurance | 10,000 |

| Equipment | 20,000 |

| Subtotal | 89,000 |

| Less: Accumulated Depreciation – Equipment | (14,000) |

| Total Assets | ₹75,000 ✔

Now liabilities:

| Liability | Cr. (INR) |

|---------|----------|

| Bill Payable | 5,000 |

| Unearned Revenue | 4,000 |

| Bank Loan | 25,000 |

| Vendor Payable | 4,000 |

| Outstanding Salaries | 5,000 |

| Accrued Expenses | 1,000 |

| Total Liabilities | ₹44,000 |

Owner's Equity:

- Owner Investments: ₹80,000

- Drawings: ₹2,000

- Net Loss: ₹27,000

→ Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000

But Total Assets = ₹75,000 → Mismatch of ₹20,000

---

## ❗️Issue Identified

There is a discrepancy. Let’s check the trial balance totals again.

From the image:

- Debit Total: ₹1,80,250

- Credit Total: ₹1,80,250 → Balanced ✔

But when we try to build the balance sheet, it doesn't balance.

Let’s re-check which items belong where.

Key Issue: Accrued Revenue (₹20,000) is not accounted for properly

- Accrued Revenue (₹20,000) is an asset — revenue earned but not yet received.

- But in the income statement, we only recorded Sales = ₹42,250

- This accrued revenue should be added to sales if it's unrecorded revenue.

Wait — Accrued Revenue is already included in Sales?

No. In accounting, Accrued Revenue is a receivable, but Sales should include all revenue earned, whether cash or accrued.

But in the trial balance, Sales = ₹42,250, and Accrued Revenue = ₹20,000 (Dr.), which is not part of Sales.

That suggests we need to adjust.

Actually, Accrued Revenue is not a revenue account — it's an asset representing revenue earned but not yet billed.

So, Sales should be adjusted upward by ₹20,000?

But wait — no, because Accrued Revenue is already recognized as revenue in the books, just not yet collected.

But in the trial balance, Accrued Revenue is listed under "Particulars" as a Dr. entry, so it's likely a receivable.

So let’s clarify:

- Accrued Revenue (Dr. ₹20,000) → It's an asset, meaning revenue has been earned but not yet invoiced.

- So Sales must include this amount.

But in the trial balance, Sales = ₹42,250, and Accrued Revenue = ₹20,000 — both are separate.

If Accrued Revenue is not part of Sales, then we must add it to Sales to reflect true revenue earned.

But that would mean Sales = ₹42,250 + ₹20,000 = ₹62,250? That seems odd.

Alternatively, Accrued Revenue might be a liability? No — it's accrued revenue, so it's an asset.

Wait — Accrued Revenue is revenue earned but not yet received → Asset

But in the trial balance, it’s shown as Dr. ₹20,000 → correct for an asset.

But Sales is already ₹42,250 — does it include this?

Possibility: Accrued Revenue is not included in Sales, so we must adjust.

But that’s not standard. Normally, Accrued Revenue is already reflected in Sales, and the Accrued Revenue account is a receivable.

So if Sales = ₹42,250, and Accrued Revenue = ₹20,000, then the company has earned ₹20,000 more than recorded?

That can’t be.

Wait — Accrued Revenue is a contra-revenue? No.

Let’s look at standard accounting:

- Accrued Revenue is an asset (e.g., services rendered but not billed).

- The corresponding revenue should be recognized in Sales.

- So if Accrued Revenue = ₹20,000, then Sales should be ₹42,250 + ₹20,000 = ₹62,250?

But in the trial balance, Sales is only ₹42,250.

So either:

- Accrued Revenue is not a new revenue, or

- Accrued Revenue is already included in Sales

But Accrued Revenue is a separate account, so it’s likely not included in Sales.

So we must adjust.

✔ Correct Approach: Adjust Sales for Accrued Revenue

In financial statements, revenue earned includes accruals.

So Sales should be:

> ₹42,250 (from trial balance) + ₹20,000 (Accrued Revenue) = ₹62,250

But wait — Accrued Revenue is an asset, not a revenue. So we don’t add it to Sales — instead, Sales should already include the revenue.

This suggests either:

- The Accrued Revenue is not additional revenue, or

- The Sales figure is incomplete.

But in the trial balance, Sales is a credit of ₹42,250, and Accrued Revenue is a debit of ₹20,000 — so they are not offsetting.

So Accrued Revenue is an asset, and Sales is revenue.

Therefore, the revenue earned is Sales + Accrued Revenue?

No — Accrued Revenue is part of revenue that is not yet recorded.

So if Accrued Revenue = ₹20,000, then Sales should be ₹42,250 + ₹20,000 = ₹62,250, but that’s not how it works.

Actually, Accrued Revenue is not a revenue account — it’s an asset.

So Sales is already the total revenue, and Accrued Revenue is a receivable.

But then why is Accrued Revenue listed separately?

Ah — perhaps Accrued Revenue is a liability? No — “Accrued Revenue” is typically an asset.

Wait — Unearned Revenue is a liability (received but not earned).

But Accrued Revenue is earned but not received → asset.

So yes, Accrued Revenue (₹20,000) is an asset.

And Sales (₹42,250) is revenue.

So total revenue is ₹42,250, and Accrued Revenue is a receivable.

But then why is Accrued Revenue not in Sundry Debtors?

Because Accrued Revenue is not yet billed, so it’s not a debtor.

So Accrued Revenue is a separate asset.

So Sales is correctly reported as ₹42,250.

Then Accrued Revenue is an asset, and Sales is revenue.

So income statement is fine.

But then balance sheet still doesn't balance.

Let’s recompute total assets:

| Asset | Amount |

|------|--------|

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation | (₹14,000) |

| Accrued Revenue | ₹20,000 |

| Total Assets | ₹95,000 ✔

Now liabilities:

| Liability | Amount |

|----------|--------|

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Bank Loan | ₹25,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Liabilities | ₹44,000 |

Owner's Equity:

- Owner Investments: ₹80,000

- Drawings: ₹2,000

- Net Loss: ₹27,000

→ Equity = ₹80,000 - ₹2,000 - ₹27,000 = ₹51,000

Total Liabilities + Equity = ₹44,000 + ₹51,000 = ₹95,000 ✔

Total Assets = ₹95,000 ✔

Perfect! Now it balances.

So the issue was missing Accrued Revenue in the asset side.

---

## ✔ Final Answer

Income Statement

| Particulars | Amount (INR) |

|------------|--------------|

| Revenue | |

| Sales | ₹42,250 |

| Total Revenue | ₹42,250 |

| | |

| Expenses | |

| Purchases | ₹30,000 |

| Insurance Charges | ₹5,000 |

| Depreciation Expense – Equipment | ₹3,000 |

| Rent | ₹15,000 |

| Maintenance Expenses | ₹3,000 |

| Mics Expenses | ₹2,000 |

| Taxes | ₹11,250 |

| Total Expenses | ₹69,250 |

| | |

| Net Loss | ₹27,000 |

---

Balance Sheet

| Assets | Amount (INR) |

|-----------|--------------|

| Current Assets | |

| Sundry Debtors | ₹15,000 |

| Prepaid Rent | ₹4,000 |

| Unexpired Insurance | ₹10,000 |

| Marketable Security | ₹10,000 |

| Accrued Revenue | ₹20,000 |

| Total Current Assets | ₹59,000 |

| | |

| Non-Current Assets | |

| Machinery | ₹30,000 |

| Equipment | ₹20,000 |

| Less: Accumulated Depreciation – Equipment | (₹14,000) |

| Net Fixed Assets | ₹36,000 |

| | |

| Total Assets | ₹95,000 |

| Liabilities & Owner's Equity | Amount (INR) |

|----------------------------------|--------------|

| Current Liabilities | |

| Bill Payable | ₹5,000 |

| Unearned Revenue | ₹4,000 |

| Vendor Payable | ₹4,000 |

| Outstanding Salaries | ₹5,000 |

| Accrued Expenses | ₹1,000 |

| Total Current Liabilities | ₹19,000 |

| | |

| Long-Term Liabilities | |

| Bank Loan | ₹25,000 |

| Total Liabilities | ₹44,000 |

| | |

| Owner's Equity | |

| Owner Investments | ₹80,000 |

| Less: Drawings | (₹2,000) |

| Less: Net Loss | (₹27,000) |

| Net Owner's Equity | ₹51,000 |

| | |

| Total Liabilities & Equity | ₹95,000 |

✔ Balances Match: ₹95,000 = ₹95,000

---

## ✔ Conclusion

- Net Loss for the year: ₹27,000

- Total Assets: ₹95,000

- Total Liabilities: ₹44,000

- Owner's Equity: ₹51,000

The key was including Accrued Revenue as an asset and ensuring all accounts were correctly classified.

Let me know if you'd like a Cash Flow Statement or Adjusting Entries!

Parent Tip: Review the logic above to help your child master the concept of trial balance worksheet example.